Residue Testing Market Size, Share, Trends, Growth and Forecast 2032

The global Residue Testing Market has emerged as a cornerstone of the modern food safety and environmental protection ecosystem. As of 2026, the market is navigating a transformative phase characterized by stringent regulatory enforcement, technological integration—specifically Artificial Intelligence (AI) and Machine Learning—and a heightened consumer demand for transparency.

This comprehensive report analyzes the market’s trajectory from its current valuation in 2026 through the forecast period ending in 2032.

1. Market Overview and Size

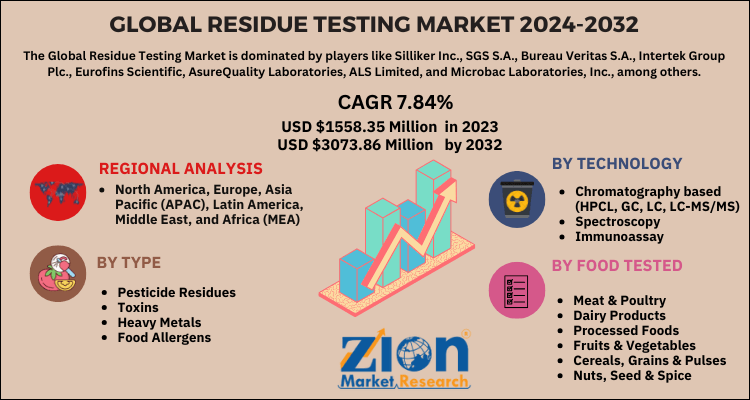

The global residue testing market was valued at approximately USD 6.12 billion in 2025 and is projected to reach USD 9.82 billion by 2032. This growth represents a steady Compound Annual Growth Rate (CAGR) of 7.0% to 8.2% over the forecast period.

The market’s expansion is primarily driven by the “Zero Tolerance” policies adopted by major economies regarding contaminants in the food supply chain. Residue testing refers to the process of detecting and quantifying traces of substances such as pesticides, veterinary drugs, heavy metals, and toxins that may remain in food, water, or soil after production and processing.

2. Market Dynamics: Drivers, Trends, and Restraints

Key Market Drivers

- Stringent Food Safety Regulations: Organizations like the European Food Safety Authority (EFSA) and the U.S. FDA (under the Food Safety Modernization Act) have implemented rigorous Maximum Residue Limits (MRLs). Non-compliance often results in costly product recalls and trade bans.

- Globalization of Food Trade: As food supply chains become increasingly global, the need for standardized testing across borders has intensified. Exporters must ensure their products meet the specific residue standards of the destination country.

- Rising Demand for Organic and “Clean-Label” Products: The shift toward organic farming has increased the demand for verification testing to ensure that “pesticide-free” claims are legitimate.

- Technological Advancements: The shift from single-residue testing to Multi-Residue Methods (MRM) allows laboratories to screen for hundreds of contaminants in a single run, drastically improving efficiency.

Emerging Trends

- AI and Automation: Leading laboratories are integrating AI-based platforms into their Liquid Chromatography-Mass Spectrometry (LC-MS/MS) workflows to automate data analysis and reduce human error.

- Rapid/On-site Testing Kits: There is a burgeoning market for portable biosensors and smartphone-compatible test kits that allow farmers and small-scale processors to conduct preliminary screenings in the field.

- Sustainability in Testing: “Green chemistry” initiatives are pushing for testing methods that require fewer solvents and less energy, aligning the laboratory industry with global ESG (Environmental, Social, and Governance) goals.

Market Restraints

- High Cost of Equipment: State-of-the-art mass spectrometry systems can cost hundreds of thousands of dollars, posing a significant barrier for small and medium-sized enterprises (SMEs).

- Lack of Harmonization: Discrepancies between MRLs in different regions (e.g., the EU vs. the US) create logistical complexities for international trade.

3. Market Segmentation

The residue testing market is segmented by the type of residue, the technology employed, and the food category being tested.

By Residue Type

- Pesticide Residues: This segment remains the largest, accounting for nearly 44% of the market share. It includes testing for herbicides, insecticides, and fungicides.

- Toxins (Mycotoxins): This is the fastest-growing segment. Mycotoxins, produced by fungi in grains and nuts, are increasingly scrutinized due to their high toxicity and the impact of climate change on fungal growth.

- Heavy Metals: Testing for lead, mercury, arsenic, and cadmium is critical in seafood and infant nutrition.

- Veterinary Drug Residues: Includes antibiotics (tetracyclines, sulfonamides) and growth hormones, primarily tested in meat, poultry, and dairy products.

By Technology

- Chromatography (LC-MS/MS and GC-MS): This is the gold standard for residue testing. LC-MS/MS (Liquid Chromatography-Mass Spectrometry) is preferred for its high sensitivity and ability to detect polar, non-volatile compounds.

- Immunoassay (ELISA): Widely used for rapid screening. While less precise than chromatography, ELISA is cost-effective and provides quick results.

- Spectroscopy: Used primarily for heavy metal detection (Atomic Absorption Spectroscopy).

By Application (Food Tested)

- Meat, Poultry, and Seafood: The largest application segment due to the high risk of antibiotic and heavy metal accumulation.

- Fruits and Vegetables: Subject to frequent pesticide testing.

- Processed Foods: Growing demand as manufacturers seek to verify the safety of complex ingredient lists.

- Cereals, Grains, and Pulses: Heavily tested for mycotoxins and pesticides.

4. Regional Analysis

| Region | Market Status | Key Growth Drivers |

| North America | Largest Market | Dominance of the U.S. market, high adoption of LC-MS/MS, and strict USDA/FDA oversight. |

| Europe | Second Largest | Strict EFSA regulations and the Rapid Alert System for Food and Feed (RASFF). |

| Asia-Pacific | Fastest Growing | Massive food exports from China, India, and Vietnam, combined with modernized domestic safety standards. |

| Latin America | Emerging | Focused on export compliance for fruits, coffee, and meat (Brazil and Argentina). |

In the Asia-Pacific region, the CAGR is expected to exceed 9% through 2032. This is fueled by the expansion of middle-class consumers who are increasingly concerned about food adulteration and the safety of domestic produce.

5. Competitive Landscape

The market is highly competitive and characterized by a mix of global testing giants and specialized regional players. Key strategies include mergers and acquisitions to expand geographic reach and investments in high-throughput automation.

Key Players include:

- SGS SA (Switzerland)

- Eurofins Scientific (Luxembourg)

- Intertek Group Plc (UK)

- Bureau Veritas (France)

- Mérieux NutriSciences (US)

- ALS Limited (Australia)

- Agilent Technologies (US – Equipment)

- Thermo Fisher Scientific (US – Equipment)

6. Conclusion and Future Outlook

The Residue Testing Market is poised for robust growth through 2032. The transition from reactive testing (responding to a recall) to proactive monitoring (integrated supply chain testing) is the most significant shift in the industry.

By 2032, we expect:

- Fully Automated Labs: Integration of robotics and AI will reduce turnaround times from days to hours.

- Blockchain Integration: Testing data will likely be linked to blockchain-based traceability systems, providing consumers with real-time safety data via QR codes.

- Wider Scope: Testing will expand beyond food to include environmental monitoring of soil and irrigation water on a routine basis.

In conclusion, stakeholders who invest in high-sensitivity multi-residue technologies and digital data management will be best positioned to lead in this $9.8 billion industry.

Read our Regional Reports >>

https://www.zionmarketresearch.com/de/report/residue-testing-market

https://www.zionmarketresearch.com/de/report/polyaluminum-chloride-market

https://www.zionmarketresearch.com/de/report/post-harvest-treatment-market

https://www.zionmarketresearch.com/de/report/biofortification-market

https://www.zionmarketresearch.com/de/report/portable-chromatography-systems-market

How to Furnish the Restaurant of your Dreams